Method for the computation of bootstrapped confidence intervals.

Usage

confidence_intervals(

data,

pred_model,

h,

train = 0.8,

M = 1000,

alpha = 0.05,

output = NULL,

...

)Arguments

- data

Data.frame (or vector) to apply cross-validation where the rows are the observations and the columns are the variables.

- pred_model

Model to predict the data where the first argument in the data and the second the length of prediction. Additional parameters can be passed using ... . Returns a vector of the predictions.

- h

Number of observations to predict into the future.

- train

Minimum amount of data (0,1) to train model. After this point, a sliding window approach is taken.

- M

Numeric. Number of bootstrap iterations.

- alpha

Significance level for the intervals

- output

Numeric or name of the column for the output when using a data.frame for

data. If not given, the first column is used.- ...

Additional parameters to pass to

pred_model.

Examples

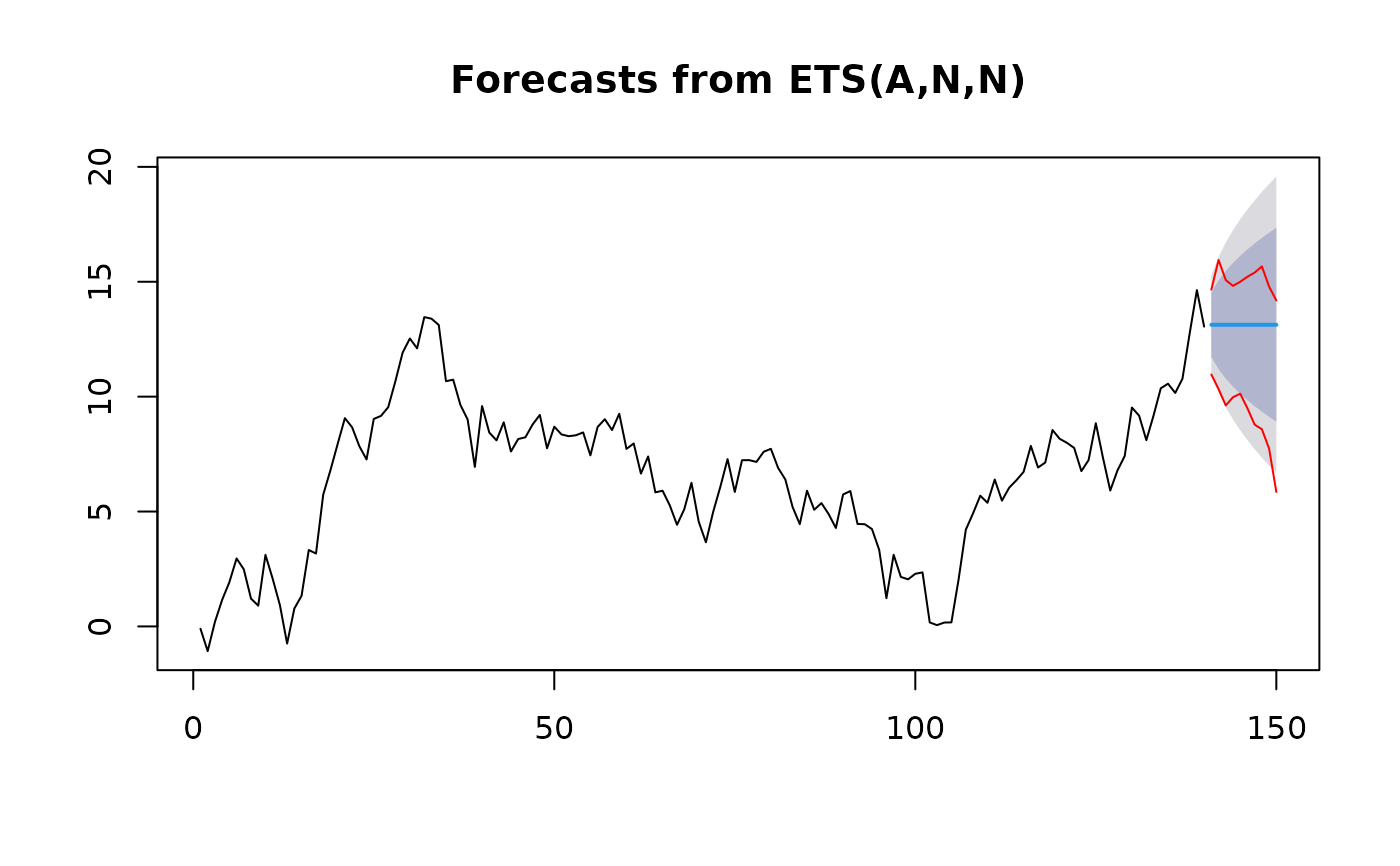

data <- cumsum(rnorm(150))

pred_model <- function(x, h) {

predict(forecast::ets(x), h = h)$mean

}

h <- 10

ets_model <- predict(forecast::ets(data[1:140]), h)

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

ints <- confidence_intervals(data = data[1:140], pred_model = pred_model, h = h)

plot(ets_model)

lines(x = 141:150, y = ints$lower, col = "red")

lines(x = 141:150, y = ints$upper, col = "red")